Description

This technical reference guide outlines the internal governance framework necessary to monitor, verify, and secure revenue streams within a hotel property.

Instead of generic bookkeeping manuals, this documentation provides a detailed operational architecture to manage sub-ledger data, audit overnight system transactions, enforce POS integrity, and supervise city ledger credit risks. The material includes dedicated reference models for credit authorization and overnight exception tracking, while offering structured closing protocols for standard and recovery month-end scenarios. Crucially, the manual defines a formal internal investigation methodology paired with a revenue fraud catalog to assist managers in identifying and documenting transaction anomalies.

Designed specifically for Financial Controllers, Income Auditors, and Directors of Finance, this guide acts as a functional blueprint to safeguard hotel assets, establish clear reporting escalation lines, and maintain strict financial independence across corporate properties.

Preview

3. FRAUD INDICATORS AND INTERNAL INVESTIGATION PROTOCOL

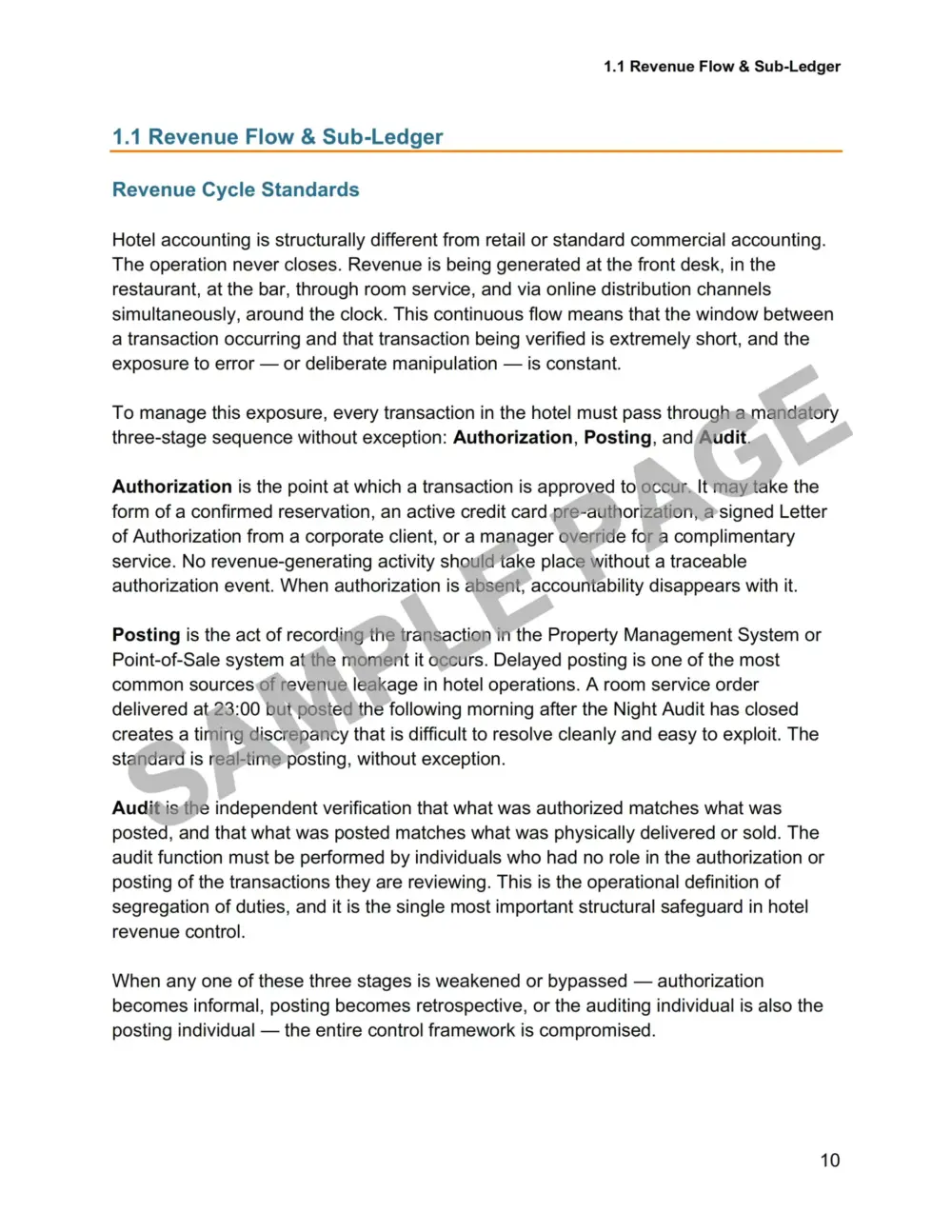

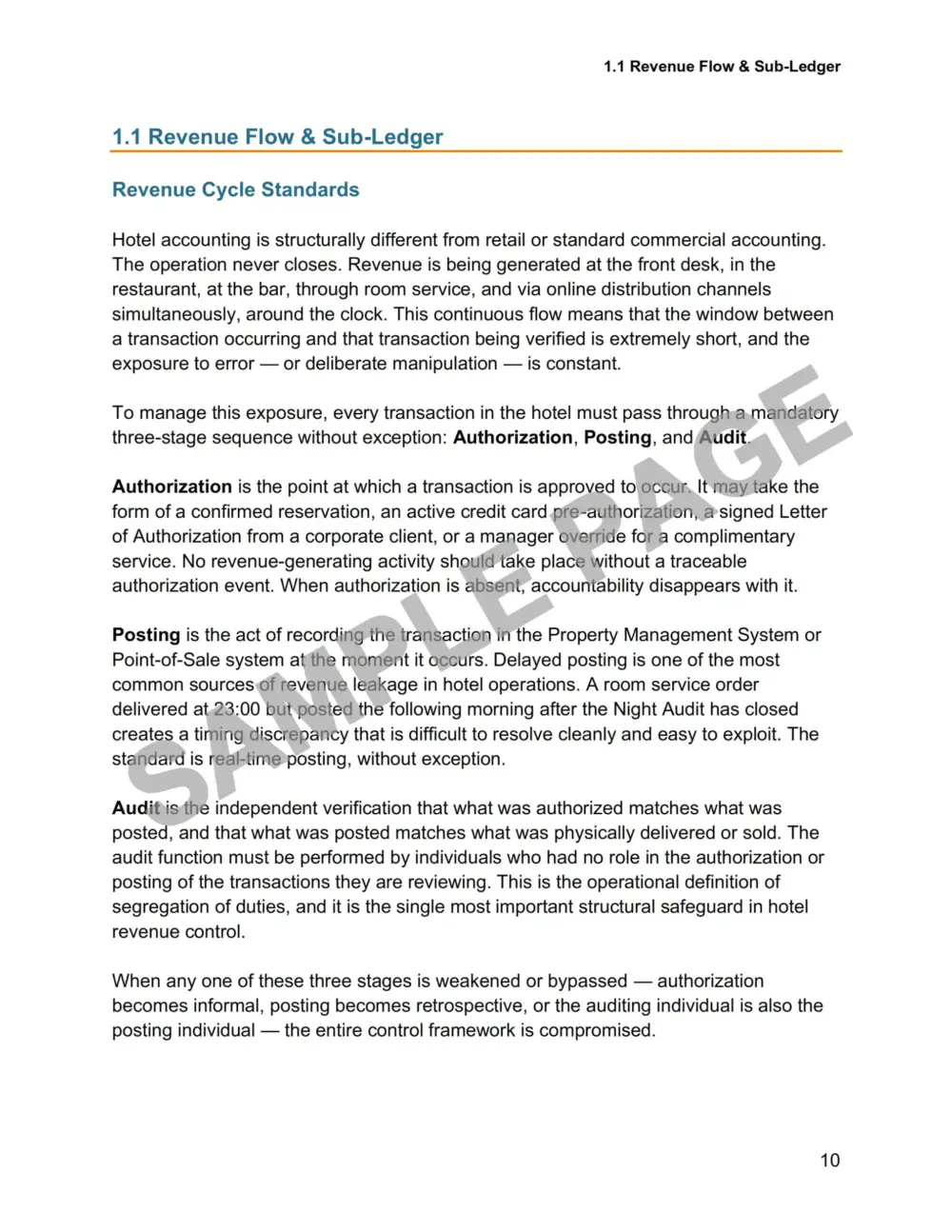

The Nature of Hotel Revenue Fraud

Internal revenue fraud in hotel operations is structurally different from fraud in most other commercial environments, and that difference shapes everything about how it must be detected and investigated. In a manufacturing company or a retail chain, revenue flows through a relatively small number of transaction types, processed by a defined group of staff, within a system whose outputs can be reconciled against physical inventory with reasonable precision. The fraud surface is bounded.

In a hotel, the fraud surface is not bounded. Revenue is generated in real time across a fragmented network of outlets — the front desk, the restaurant, the bar, room service, the spa, the business center, banquet operations — by staff who work rotating shifts, handle multiple transaction types simultaneously, and operate within a culture of discretionary service where exceptions, adjustments, and complimentary gestures are a routine part of the guest experience. That culture of discretion, which is genuinely necessary for hospitality operations, is also the environment in which fraud finds its most natural cover.

The consequence is that hotel revenue fraud is rarely a single dramatic event. It is almost always a pattern — a sustained series of small, individually defensible transactions that collectively represent a material financial loss. A void ratio that is slightly elevated. A cash drawer that opens slightly more often than the transaction volume justifies. A COMP room that appears on the exception report slightly more regularly than the authorization process should allow. None of these signals, taken in isolation, constitutes proof of fraud. Each of them, taken in context and analyzed against the control framework described in Part One of this manual, is a diagnostic indicator that requires investigation.

The Financial Controller’s role in fraud detection is therefore primarily analytical. It is not to catch people in the act — that rarely happens in a well-controlled property because the act is too fragmented and too incremental to be caught in real time. It is to recognize patterns in financial data that are inconsistent with legitimate operational activity, to investigate those patterns with sufficient rigor to distinguish fraud from error, and to respond with a process that is legally defensible, professionally appropriate, and organizationally sustainable. This chapter provides the framework for all three of those responsibilities.